Slowing Growth Begins to Test Holly Springs’ (NC) Low-Tax Model

A financial structure supported by a small group of high-value taxpayers has helped keep rates low, but rising costs and moderating revenue are narrowing the town’s margin for future decisions

Holly Springs, NC, Apr. 15, 2026 — Holly Springs officials opened early discussions on the Fiscal Year 2027 (FY27) budget Tuesday night with a clear signal that the town’s financial model is entering a more constrained phase. Revenues are still growing, but more slowly, just as long-term costs tied to parks, public safety, and infrastructure are accelerating.

At the center of the conversation was property tax revenue, which accounts for roughly half of the town’s general fund. That operating budget, which totals about $60 million within a roughly $117 million overall budget, supports day-to-day services such as police, fire protection, parks, planning, and administration. The ability to maintain those services depends heavily on steady year-over-year revenue growth.

Staff reported that growth in that revenue stream is coming in about $1.7 million below what had been typical in recent years. It is not a decline, but it represents a meaningful slowdown. Where Holly Springs had previously seen annual growth in the 6 percent to 8 percent range, projections now sit closer to 4.5 percent. Without recent economic development gains, that number could be similar to the 1 percent to 2 percent growth experienced by peer communities across Wake County.

That shift matters because most of the town’s costs are recurring and difficult to reduce. Personnel costs in particular continue to rise, and expenses tied to public safety, parks, and ongoing services increase as the town grows.

A Financial Model Built on Growth and Concentration

What makes Holly Springs different is not its reliance on property taxes, but how that revenue is structured.

The town maintains one of the lowest municipal tax rates in Wake County, currently the second lowest, a position built in part on a highly concentrated tax base. A small number of large taxpayers, primarily in the biotech sector, account for a significant share of total revenue. The town’s top three taxpayers alone contribute more than 16 percent of all property tax revenue.

That structure has allowed Holly Springs to hold its tax rate relatively low, even as it kept the rate flat through multiple years of inflation and growth. At the same time, it creates sensitivity. Changes in valuation, successful tax appeals, or shifts affecting those large properties can have an outsized impact on the town’s finances.

Against that backdrop, staff framed the FY27 budget around a balancing act between affordability, maintaining service levels, and investing in new programs and infrastructure. “Affordability, maintain service levels, and then new programs and infrastructure” was how one official described the challenge.

Slower Growth Meets Rising Long-Term Costs

The timing of the slowdown is significant because several high, unavoidable costs are approaching.

Beginning in FY28, Eagles Landing Park is expected to add between $2 million and $2.5 million annually to the operating budget. Within a few years, Fire Station 4 will require hiring between 12 and 24 firefighters along with equipment, creating another roughly $2 million annual impact. Fire Station 5 follows shortly after, with similar costs projected in the early 2030s.

Those figures stand against a backdrop in which annual general fund revenue growth typically ranges from $4 million to $5 million. In practical terms, a single major initiative could absorb a substantial portion of new revenue in a given year, limiting flexibility for other priorities.

“You can imagine if two million went out of the gate… what that means for other initiatives,” staff told council.

Rethinking How the Town Funds Itself

A significant portion of the workshop focused on restructuring how Holly Springs funds smaller capital projects, an issue that sits directly at the intersection of operating services and long-term planning.

Currently, the town relies heavily on PAYGO, or pay-as-you-go funding, using operating budget dollars to fund smaller capital needs such as sidewalks, facility repairs, and equipment replacements. That approach has worked during years of strong growth, but it now creates pressure because it draws from the same pool that funds core services.

Under the proposed FY27 approach, the town would begin shifting those funding sources. Street and sidewalk projects would be funded more directly through vehicle fee revenues tied to transportation uses. Facility maintenance would move toward the capital side of the budget, funded through property tax allocations designated for long-term investments. Programmatic efforts such as downtown grants would remain within the operating budget.

The goal is to better align funding sources with their intended use while freeing up operating dollars to maintain service levels. It also reflects a broader shift in strategy as the town moves away from relying on periodic fund balance infusions to cover maintenance needs.

That shift is being driven, in part, by the condition of the town's facilities. “Our facilities are getting of a certain age,” staff noted, pointing to known lifecycle replacement needs across multiple sites.

Using Fund Balance to Address Immediate Needs

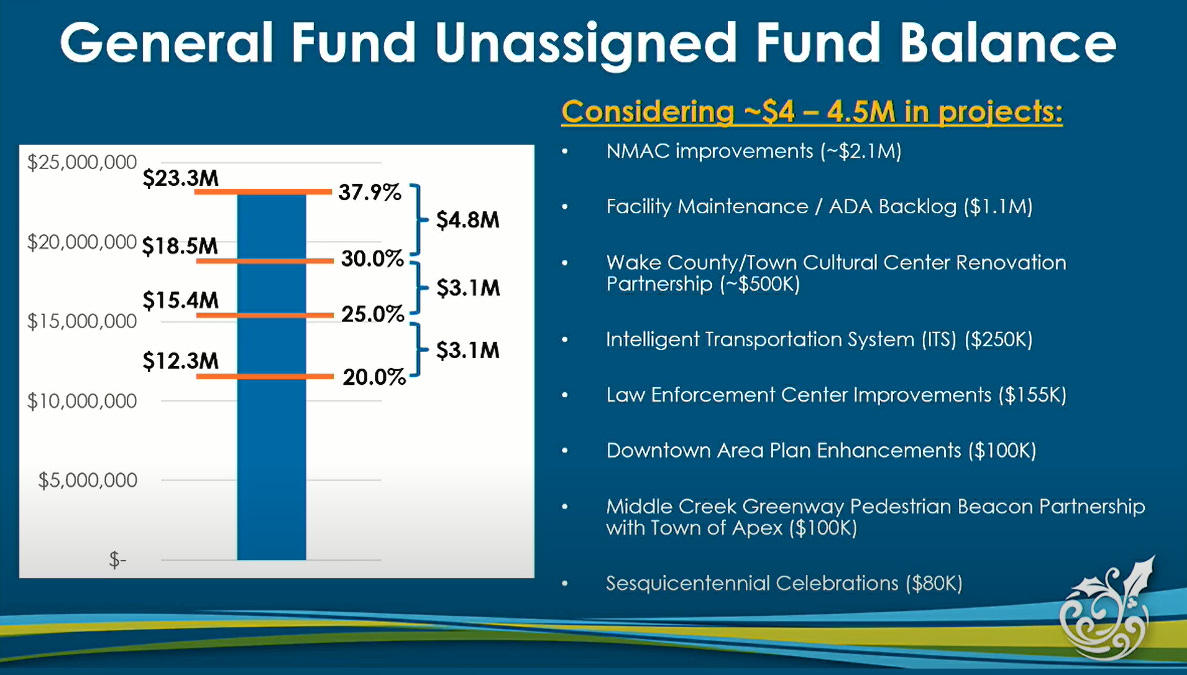

With Holly Springs’ General Fund balance at $23.3 million, well above its policy target of $18.5 million, the town is considering allocating roughly $4 million to $5 million to one-time investments. The largest allocation, approximately $2 million, would serve as the town’s match for Wake County hospitality tax funding tied to improvements at the North Main Athletic Complex. Planned upgrades include parking lot rehabilitation, turf replacement, a new scoreboard, and HVAC and mechanical system improvements.

Additional allocations would address $1.1 million in facility maintenance and ADA backlog, Cultural Center renovations under a joint agreement with Wake County, early investment in an Intelligent Transportation System, and smaller projects including downtown enhancements, greenway infrastructure, and public safety facility upgrades.

These investments highlight the distinction between the town’s operating and capital budgets. The operating budget funds ongoing services, while capital spending focuses on maintaining and building long-term infrastructure.

Planning for Infrastructure and Its Ongoing Costs

The town’s capital planning strategy is built on a forward-investment model in which infrastructure is constructed ahead of demand to support future growth. That includes water and wastewater capacity, transportation systems, and parks.

While those investments enable growth, they also create long-term obligations. Every new facility brings ongoing operating costs, including staffing, maintenance, and utilities, that must be absorbed into future budgets.

This dynamic was evident in discussions around the town’s traffic signal system, which is currently managed by NCDOT. Transitioning to local control would require new staffing, technology, and infrastructure investments, with future costs estimated at around $1 million. “We don’t have any staff expertise on how to run a traffic management,” staff said, emphasizing the need for careful planning before taking on that responsibility.

A Narrowing Margin for Future Decisions

As the workshop concluded, the underlying theme remained consistent. Holly Springs is not facing a financial crisis, but it is entering a period in which financial decisions will be more constrained.

The town’s financial model, built on property value growth, population expansion, and long-term infrastructure investment, continues to function, but with less margin for error. Revenue growth is moderating. Costs are rising. And the structure of the tax base introduces both strength and sensitivity.

“There’s only so much that’s reasonably… to expect our residents… to fund their government,” staff said.

The FY27 budget recommendation will be formally presented on May 12th, followed by a public hearing on May 19th and potential adoption on June 2nd.

Maybe need to hold off on revamping Ting Park. We know we have to have water , wastewater , firefighter and police personnel.

Not sure the cost of the recreation renovations makes sense.

We would like Mims Property to become a designated historic preserve. This will prevent the planned development (& avoid the demolition of much of this forest). Keeping this entire property as a preserve means lower cost to taxpayers. It will be a never-ending money pit for taxpayers if the town builds and maintains an amphitheater, a large “community” building, grass fields (frequent fertilizer, pesticide, herbicide, and mowing), entertainment equipment, artificial lighting (& cost to run those lights), so on. Not to mention the environmental damage it will cause. According to NC natural habitat documentation, the downtown area already has over 20% impervious surfaces with the Mims Property acting as the one last carbon sink, the one last continuous tree canopy with undamaged rolling hills that buffer noise pollution, light pollution, and air pollution. It would be such an expense and such a tragedy for future generations to lose even a few acres of this documented historic property. Forests aren’t a placeholder. They are a vital part of our ecosystem.